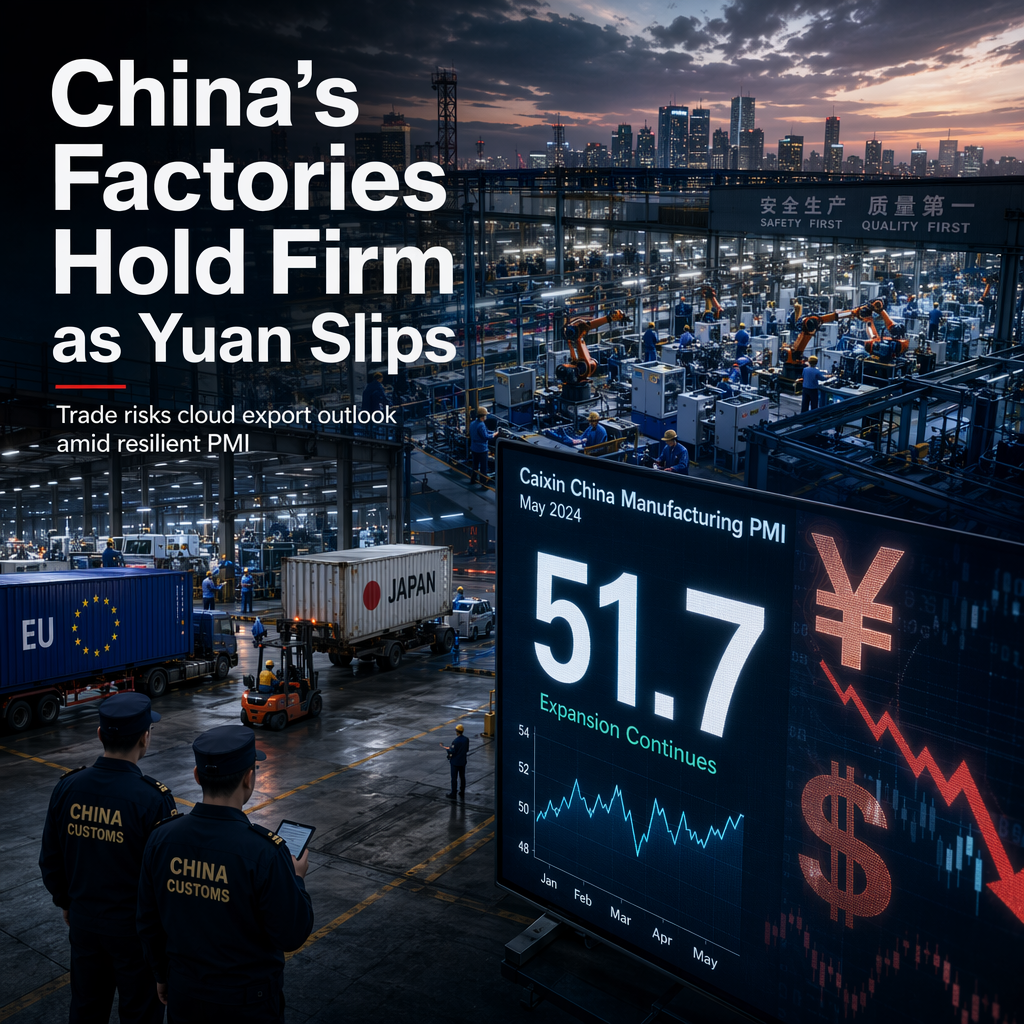

China's private sector manufacturing PMI for June registered at 51.7, marking a three-month low but still slightly above Commerzbank's estimate of 51.5 and only marginally down from May's 51.8. This result capped the strongest quarter for the sector in nearly six years, according to Commerzbank analysts Charlie Lay and Dr. Henry Hao [1]. The official NBS manufacturing PMI also surpassed expectations, coming in at 50.3 versus a consensus of 50.1, while the non-manufacturing PMI surprised to the upside at 50.2 [1]. These data points indicate that China's export-driven industrial sector continues to maintain momentum despite ongoing structural challenges in the broader economy [1].

However, Commerzbank warns that growing external trade frictions, particularly from the European Union and Japan, are emerging as significant downside risks to China's export outlook for the second half of the year. The European Union has recently implemented measures targeting Chinese steel imports and small-parcel e-commerce shipments, which could further pressure export growth [1].

In the foreign exchange market, the Chinese yuan weakened despite a stronger fixing by the People's Bank of China (PBoC). The USD/CNY pair rose by 70 pips to 6.79, and the offshore USD/CNH increased by 80 pips to 6.80. This depreciation was attributed to broad U.S. dollar strength following remarks by Federal Reserve Chair Kevin Warsh at the ECB forum [1].

No forward-looking analyst opinions beyond the warning of trade-related downside risks were provided in the source article.

CONCLUSION

China's manufacturing sector demonstrated resilience in the latest PMI readings, but the yuan weakened as external trade risks intensified. Market sentiment remains cautious, with analysts highlighting the potential for further export headwinds in the second half of the year due to new trade measures from the EU and Japan.