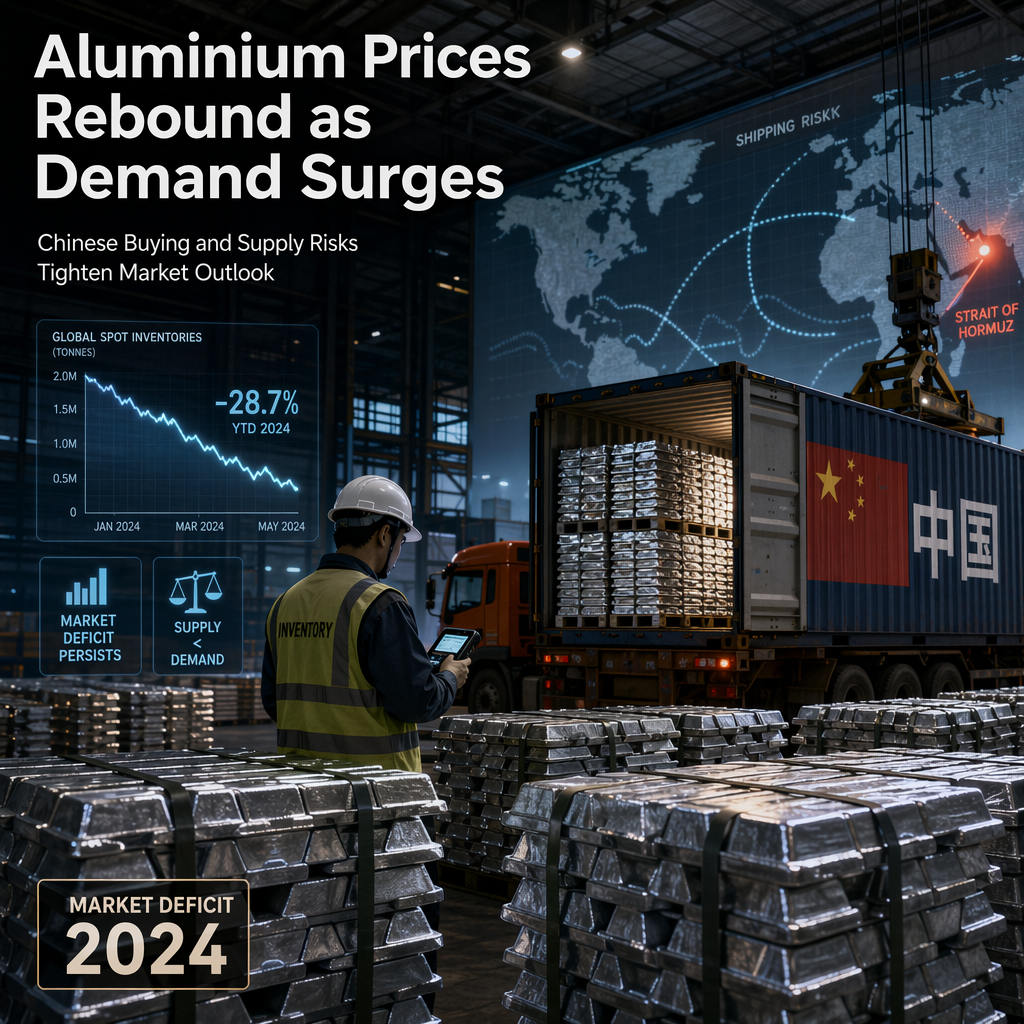

Aluminium prices have rebounded for a second consecutive session after reaching a four-month low, driven by renewed buying interest from China as lower prices attracted demand [1]. The market had previously faced downward pressure due to a faster-than-expected recovery in Middle Eastern supply following a ceasefire, but ING analysts Warren Patterson and Ewa Manthey maintain that the aluminium market is still expected to remain in deficit this year [1].

A key supporting factor for the constructive outlook is the continued decline in China's aluminium spot inventories, which have fallen for a twelfth straight session to 1.09 million tonnes, representing a drop of more than 25% from their April peak [1]. Additionally, renewed attacks on vessels near the Strait of Hormuz have heightened shipping risk concerns, potentially impacting supply chains [1].

Despite these supportive fundamentals, speculative sentiment in the aluminium market has weakened. The latest Commitment of Traders Report (COTR) data shows that net long positions in LME aluminium fell by 14,891 lots for the fourth consecutive week, reaching 53,923 lots as of the week ending 3 July—the lowest level since May 2019 [1].

CONCLUSION

Aluminium prices are recovering as Chinese demand picks up and inventories decline, supporting expectations of a market deficit this year. However, speculative sentiment remains weak, and ongoing geopolitical risks could influence future market dynamics.