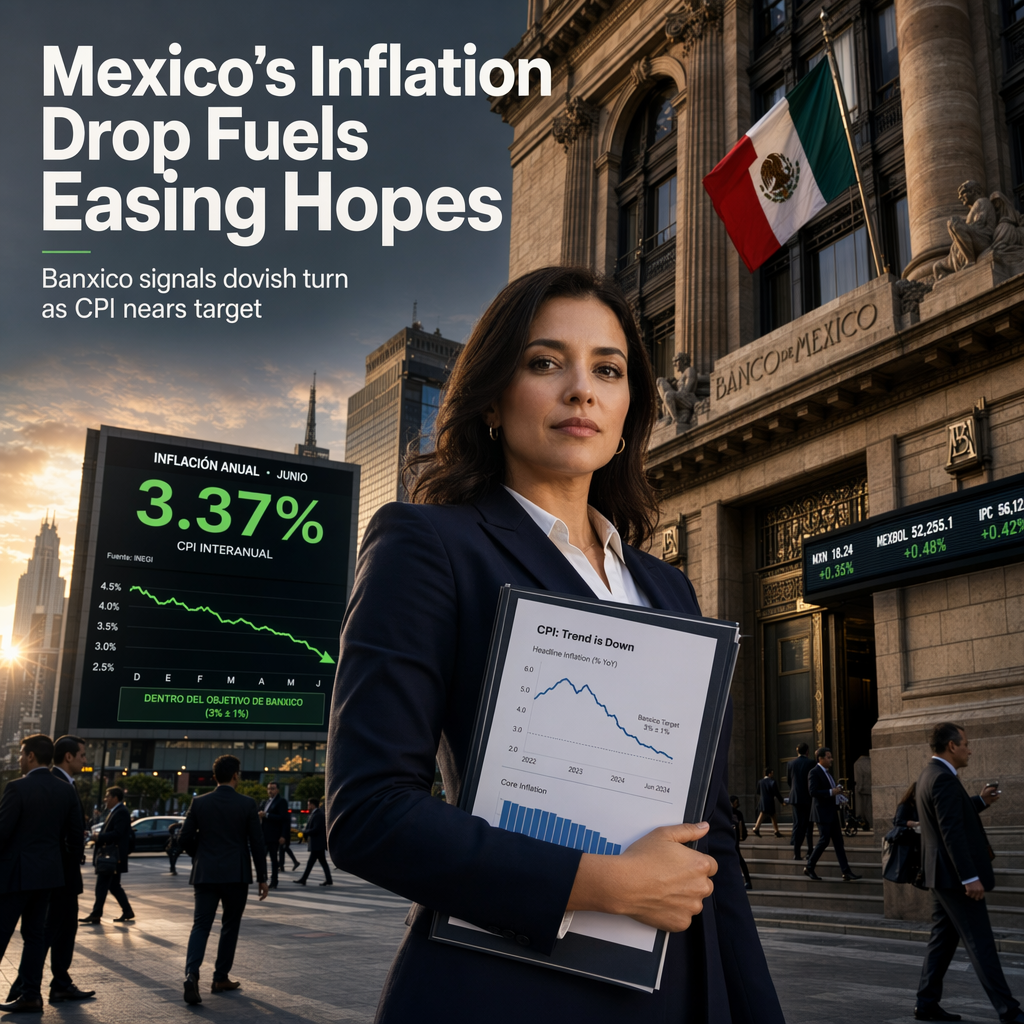

Mexico's June inflation data surprised to the downside, with headline CPI falling to 3.37% year-over-year and core inflation to 4.03% year-over-year, according to Societe Generale analysts Dev Ashish and Brendan McKenna [1]. The second bi-weekly reading showed headline inflation at 3.18% year-over-year and core at 3.94% year-over-year, bringing both measures close to or within Banxico’s target range and providing strong evidence that underlying inflation pressures are easing [1].

Services inflation (excluding housing and education) moderated to 4.40%, while core goods inflation eased to 3.45%, indicating that weak economic activity is beginning to weigh on domestic pricing power and supporting Banxico’s expectation that demand weakness would drive disinflation [1]. Non-core inflation remains highly supportive, with falling prices of seasonal food items and livestock likely to push headline inflation even lower through July-August. Societe Generale analysts suggest that some bi-weekly headline readings could temporarily fall below Banxico’s 3.0% target [1].

Looking ahead, Societe Generale expects headline inflation to end 2026 at 3.69% year-over-year and 3.62% year-over-year in 2027, while core inflation is projected to moderate to around 3.46% next year. Future disinflation is expected to be increasingly driven by core components, particularly services [1].

The softer inflation profile strengthens the case for a more dovish Banxico stance, but analysts do not anticipate immediate rate cuts. The policy rate is expected to remain at 6.50% in the near term, with a 40% probability of a cut in the third quarter of 2026 and a potential 50 basis point easing cycle by the first half of 2027 if inflation continues to surprise lower and the growth backdrop remains weak [1].

CONCLUSION

Mexico's softer June inflation data has reinforced expectations for a more dovish Banxico policy stance, though immediate rate cuts are not anticipated. The policy rate is likely to remain at 6.50% in the near term, with potential easing considered for 2026-2027 if disinflation persists and economic growth remains subdued. This development signals a supportive environment for further monetary easing, contingent on continued inflation moderation.