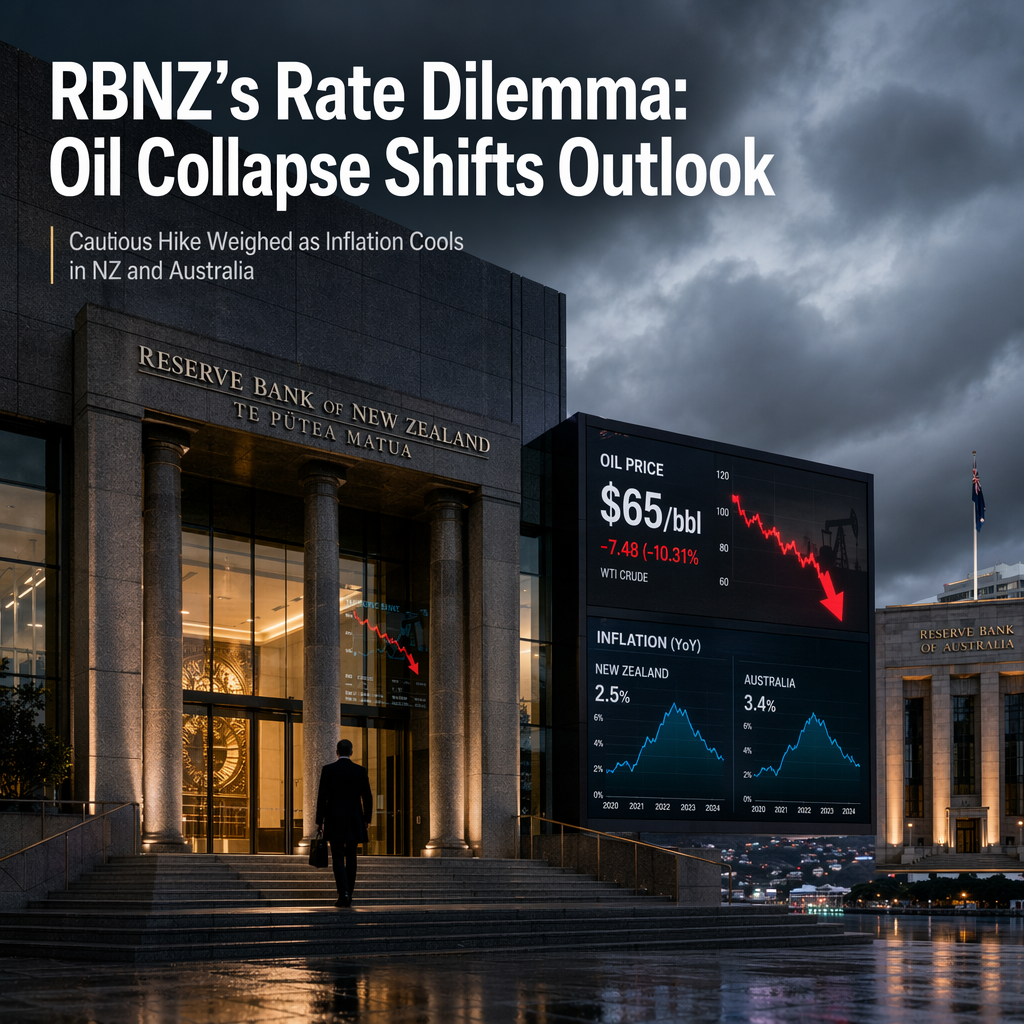

The Reserve Bank of New Zealand (RBNZ) is expected by ING’s Francesco Pesole to deliver a 25 basis point 'insurance' rate hike in July, raising the policy rate to 2.50%, despite a sharp drop in oil prices and softer inflation data. Pesole notes that the RBNZ’s May rate projections, which anticipated 50-75bp of tightening by the end of 2026, have been largely invalidated by the recent decline in oil prices and lower inflation, making the upcoming decision more finely balanced. The RBNZ previously kept rates on hold at 2.25% in May, with Governor Anna Breman casting the tiebreaking vote in a 3-3 split decision, citing concerns about inflation expectations and second-round effects. However, the RBNZ’s earlier assumptions of Dubai crude at $95-105/bbl for the rest of 2026 now contrast sharply with current levels near $65, rendering projections for headline CPI above 4.0% until Q4 2026 unrealistic. ING expects the 25bp hike to be similar to the ECB’s June 'insurance' move, but warns that the risk of this being a one-off hike has increased, which could limit further support for the New Zealand Dollar (NZD) [1].

In Australia, BNY’s Geoff Yu reports that the Melbourne Institute inflation gauge fell 0.4% month-on-month in June, following a 0.3% decline in May, marking the second consecutive month of price weakness. The year-on-year rate slowed to 3.9% from 4.4%, while the trimmed mean measure fell 0.5% month-on-month after a 0.1% drop previously, bringing its year-on-year pace down to 2.8% from 3.6%. This broad-based easing in both headline and underlying price pressures suggests that disinflation is becoming more established in Australia. As a result, Yu suggests that the Reserve Bank of Australia (RBA) may need to move away from its neutral stance, with current market pricing for 35bp of tightening by year-end now appearing increasingly vulnerable if the softer inflation trend persists [2].

While the RBNZ is considering a cautious rate hike to anchor inflation expectations, the RBA faces growing pressure to reconsider further tightening as disinflation takes hold. Both central banks are responding to rapidly changing inflation dynamics, with market expectations adjusting accordingly.

CONCLUSION

The RBNZ is likely to deliver a cautious rate hike in July, but the move may be a one-off due to lower oil prices and softer inflation, limiting NZD upside. Meanwhile, persistent disinflation in Australia is undermining expectations for further RBA tightening, highlighting the shifting monetary policy landscape in both countries.