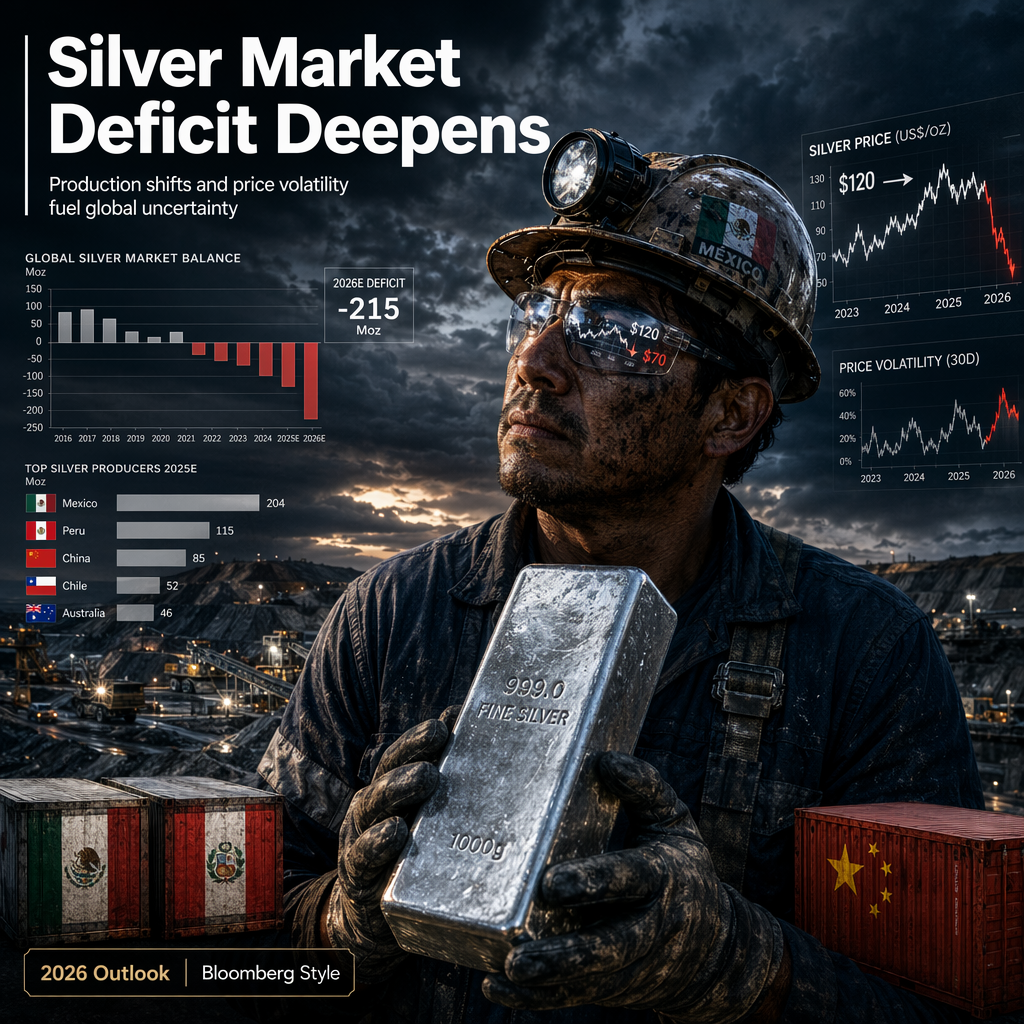

The global silver market is experiencing significant structural changes, with half of the world's mined silver now coming from just three countries: Mexico, Peru, and China. According to data from The Silver Institute, Mexico produced approximately 173 million ounces of silver in 2025, accounting for about one-fifth of global output. Peru followed with 130 million ounces, and China produced 113 million ounces. Notably, Mexico's output declined by 5% for the third consecutive year, while Peru's production increased by 7%, narrowing the gap between the two countries. Russia also saw a substantial 23% jump in production, moving it to fourth place globally. Regionally, North American silver output fell by 3% to its lowest level in a decade, whereas Central and South America saw a 5% increase, underscoring the Americas' continued dominance in global supply, particularly Mexico and Peru [1].

Despite these shifts in production, the silver market remains under pressure due to ongoing structural deficits. The market posted a deficit of 40.3 million ounces in 2025, marking the fifth consecutive year of shortfall, and this gap is expected to widen to 46.3 million ounces in 2026. This persistent deficit comes even as supply rises and demand contracts slightly. The Silver Institute's World Silver Survey 2026 highlights that the January 2026 rally, which saw silver prices surge to an all-time high above $120 before correcting to around $70, was driven by robust physical investment demand, particularly in coins and bars, leading to product shortages and a surge in Exchange-Traded Product (ETP) inflows [1].

Analysts from The Silver Institute maintain a constructive outlook for silver, anticipating only a mild decline in both demand and production. However, they warn that the market is set for a sixth consecutive deficit in 2026, which, combined with high ETP holdings and the potential for metal to flow back to the CME if positioning recovers, could further pressure inventories. The cumulative drawdown of stocks over recent years has made the market increasingly vulnerable to liquidity squeezes. The report notes that while such squeezes may not be constant, lower liquidity compared to previous years is likely to result in continued volatility in both prices and lease rates [1].

CONCLUSION

The silver market is grappling with ongoing supply deficits, shifting production dynamics, and heightened price volatility. With inventories under pressure and liquidity concerns mounting, analysts foresee continued market instability and potential for further price swings. Investors and market participants should remain alert to these evolving trends.