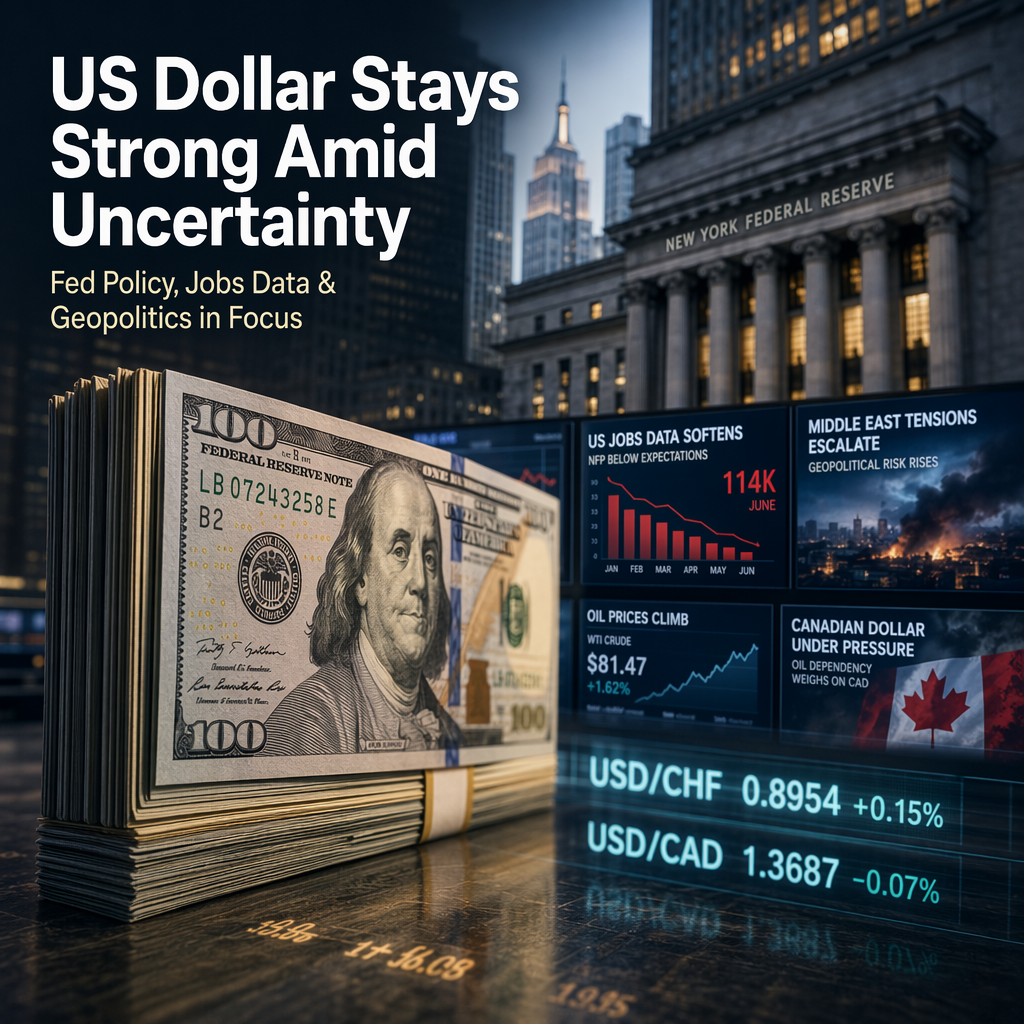

The US Dollar (USD) maintained its strength on Tuesday, supported by a hawkish outlook from the Federal Reserve (Fed) and renewed geopolitical tensions, despite softer US labor market data. The USD/CHF pair traded around 0.8066, marking its second consecutive day of gains, while the US Dollar Index (DXY) hovered near 100.95, reflecting the Greenback's resilience against a basket of major currencies [1]. The four-week average of the ADP Employment Change eased to 21K from 24.25K, and the June Nonfarm Payrolls (NFP) report showed only 57K jobs added, well below the expected 110K, signaling a gradual cooling in the US labor market [1][2].

Fed officials, including New York Fed President John Williams and Governor Christopher Waller, reiterated concerns about persistent inflation and emphasized the central bank's commitment to its 2% inflation target. Williams described the risks to the labor market as 'pretty balanced' and stated that monetary policy is 'well positioned' or 'in a good place' to achieve the Fed's goals [1][2]. According to the CME FedWatch Tool, there is a 75% probability that the Fed will keep rates unchanged at the upcoming July meeting, while the odds of a September rate hike have decreased to 58% from 68% a week ago [1][2].

Geopolitical risks also influenced market sentiment, as Iran's Islamic Revolutionary Guard Corps (IRGC) reportedly attacked a commercial vessel near the Strait of Hormuz, providing additional support to the US Dollar and boosting oil prices. West Texas Intermediate (WTI) crude rose 2.47% to around $70.30 per barrel, benefiting oil-exporting countries like Canada [1][2].

In Canada, the Canadian Dollar (CAD) held steady, with the USD/CAD pair trading near 1.4205. Stronger-than-expected Canadian trade data showed merchandise exports rising 0.9% in May and imports falling 0.2%, widening the trade surplus to CAD$4.24B from CAD$3.41B in April. The Ivey PMI eased to 59.7 from 61.3 but remained in expansion territory. Despite these positive domestic indicators and higher oil prices, the CAD struggled to gain traction, with analysts from Scotiabank, RBC, Societe Generale, and NBC suggesting that the Canadian Dollar's near-term upside is limited [2].

Market participants are now awaiting the release of the Federal Open Market Committee (FOMC) meeting minutes on Wednesday, which could provide further clarity on the Fed's policy direction and impact the trajectory of both the US Dollar and major currency pairs such as USD/CHF and USD/CAD [1][2].

CONCLUSION

Despite softer US labor data, the US Dollar remains supported by hawkish Fed commentary and heightened geopolitical tensions. While Canadian economic data and higher oil prices offer some support to the CAD, analysts see limited upside in the near term. Investors are focused on the upcoming FOMC minutes for further guidance on US monetary policy.