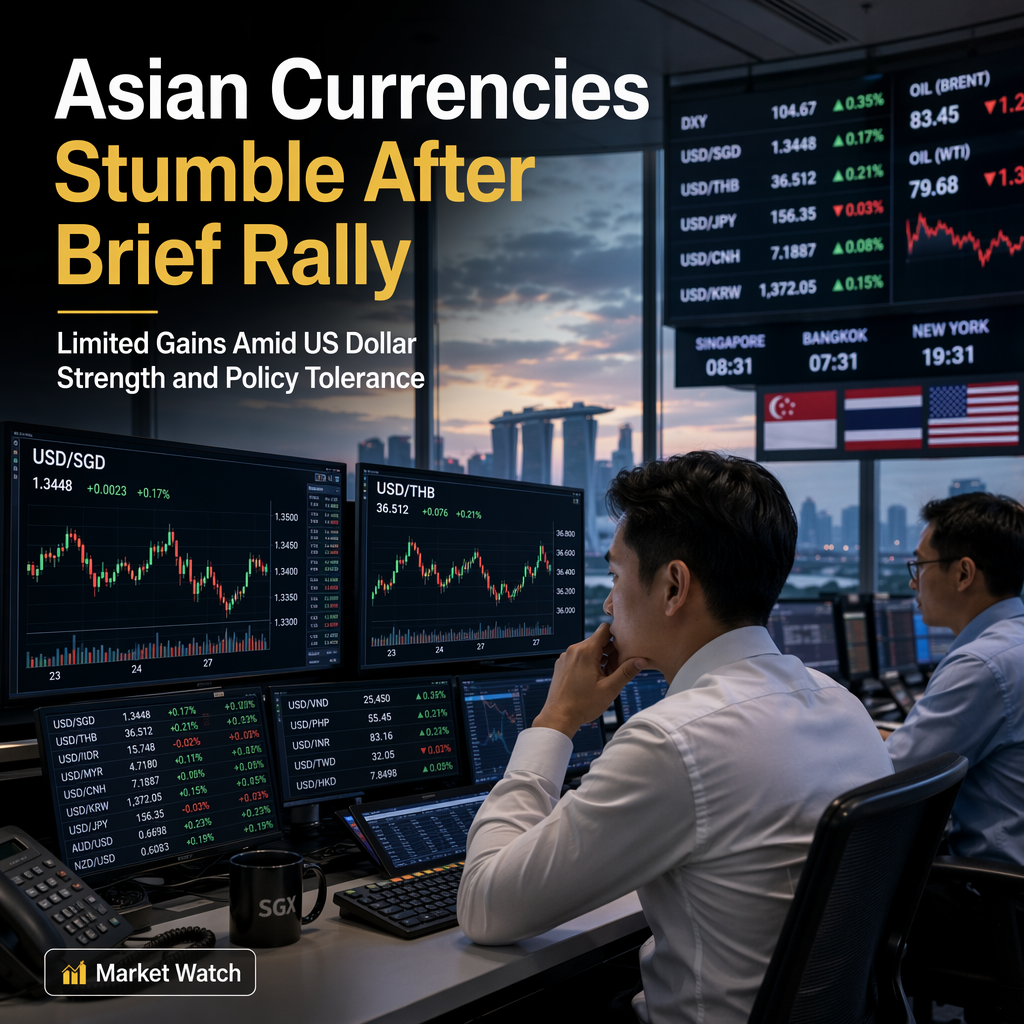

Following the release of softer United States Consumer Price Index (CPI) data, both the Singapore Dollar (SGD) and Thai Baht (THB) experienced brief gains against the US Dollar (USD), but these moves were quickly retraced, indicating limited follow-through in local currency strength [1][2]. For the Singapore Dollar, United Overseas Bank (UOB) analysts Quek Ser Leang and Lee Sue Ann observed that the USD/SGD pair reversed its New York-session plunge and closed near 1.2910. Their SGD Nominal Effective Exchange Rate (NEER) model suggests the currency will remain 1.50–2.00% above midpoint, implying an intraday USD/SGD range of 1.2874–1.2939. In the short term, they expect consolidation within 1.2885–1.2930, and over the next 1-3 weeks, they see limited downside risk, with the pair likely to stay within a 1.2860–1.2955 range [1].

Similarly, OCBC analysts Sim Moh Siong and Christopher Wong noted that the USD/THB pair fell after the US CPI release but quickly retraced, signaling limited gains for the Thai Baht. They attribute this to elevated oil prices, an uneven tourism recovery, and the Bank of Thailand's (BoT) apparent policy tolerance for orderly THB weakness. BoT Governor Vitai Ratanakorn's recent remarks indicated no immediate discomfort with the currency's depreciation, which is seen as supporting Thailand’s exports and tourism. However, the BoT would likely intervene if volatility became excessive [2].

OCBC analysts suggest that while the THB may recover alongside broader Asian currencies if USD softness persists, its gains could lag due to persistent headwinds such as high oil prices. They recommend buying USD/THB on dips around 33.40–33.20, with the pair last seen at 33.50 [2].

Overall, both currencies are expected to trade within tight ranges in the near term, with policy stances and external factors such as oil prices and tourism trends influencing their trajectories [1][2].

CONCLUSION

Both the Singapore Dollar and Thai Baht showed only limited and short-lived gains against the US Dollar following softer US CPI data, with analysts expecting continued consolidation and policy tolerance for mild depreciation. Market participants are advised to watch for further USD movements and external factors such as oil prices, as these will likely dictate the pace and direction of Asian currency moves in the near term.