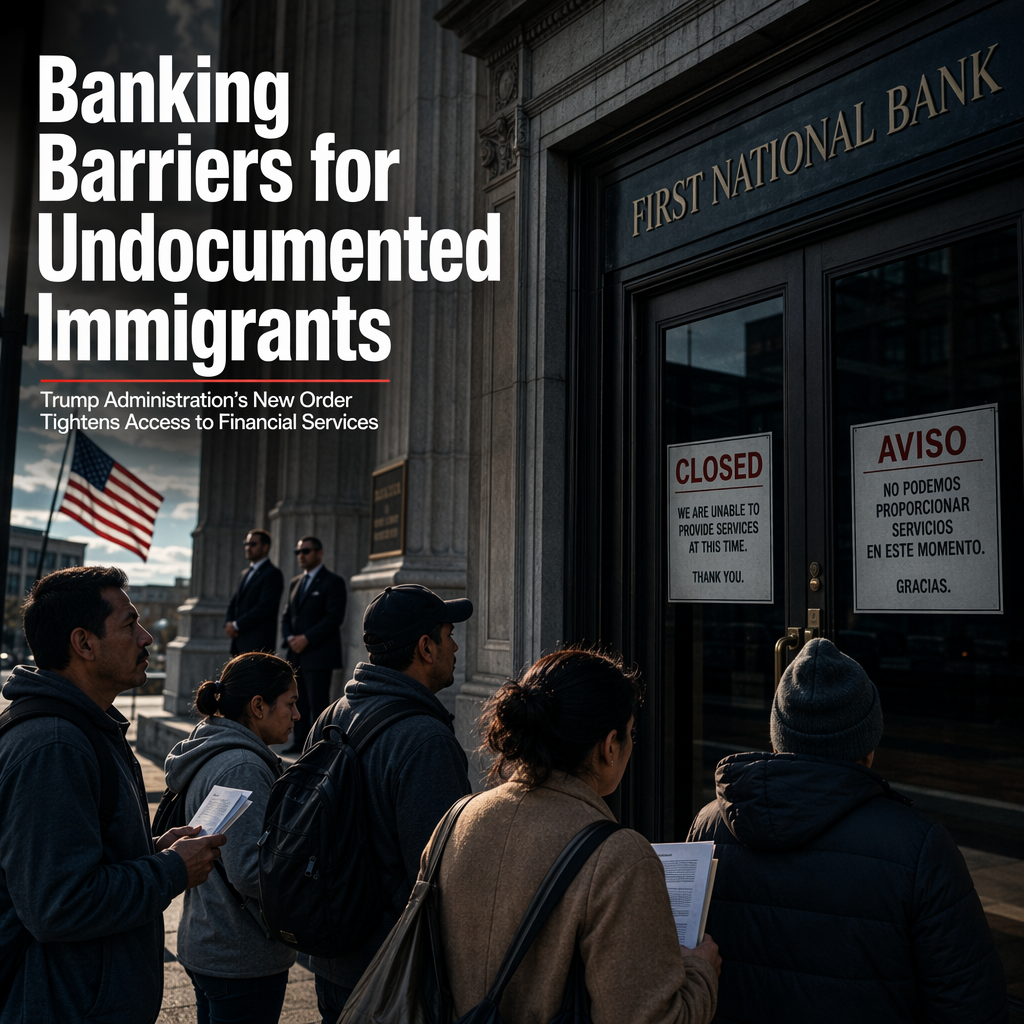

The Trump administration is advancing a policy aimed at restricting access to banking services for illegal immigrants, according to White House deputy chief of staff Stephen Miller. Miller stated that the administration's goal is to 'debank illegal immigrants' as a means to incentivize self-deportation from the United States. He referenced an executive order signed by President Trump on May 19, which directs banks and federal regulators to increase scrutiny of accounts and credit applications involving immigrants without legal status or work authorization [1].

While the executive order does not explicitly instruct banks to deny credit cards or bank accounts to illegal immigrants, Miller noted that compliance with the order could make it more difficult for these individuals to participate in the U.S. financial system. He emphasized that illegal immigrants currently have access to credit cards, bank accounts, and direct deposit, and that shutting down these avenues would serve as a 'massive engine for deportation' [1].

Federal agencies have already begun implementing the executive order. In early June, the Consumer Financial Protection Bureau, led by Russell Vought, issued guidance stating that lenders may—and in some cases must—consider applicants' immigration status and work authorization when assessing their ability to repay loans. Additionally, on July 13, three federal agencies issued guidance reminding supervised financial institutions to apply existing safe-and-sound credit risk management practices when lending to borrowers who are not legally authorized to work in the United States. Both advisories indicate that illegal immigrants could be considered higher-risk customers for loans [1].

The policy is expected to impact the ability of illegal immigrants to access financial services, though the full market reaction and long-term implications were not detailed in the source article [1].

CONCLUSION

The Trump administration's new policy is set to make it more difficult for illegal immigrants to access banking services, with federal agencies already issuing guidance to financial institutions. While the immediate market impact is not fully clear, the move signals increased regulatory scrutiny and potential changes in risk assessment for banks dealing with undocumented borrowers.