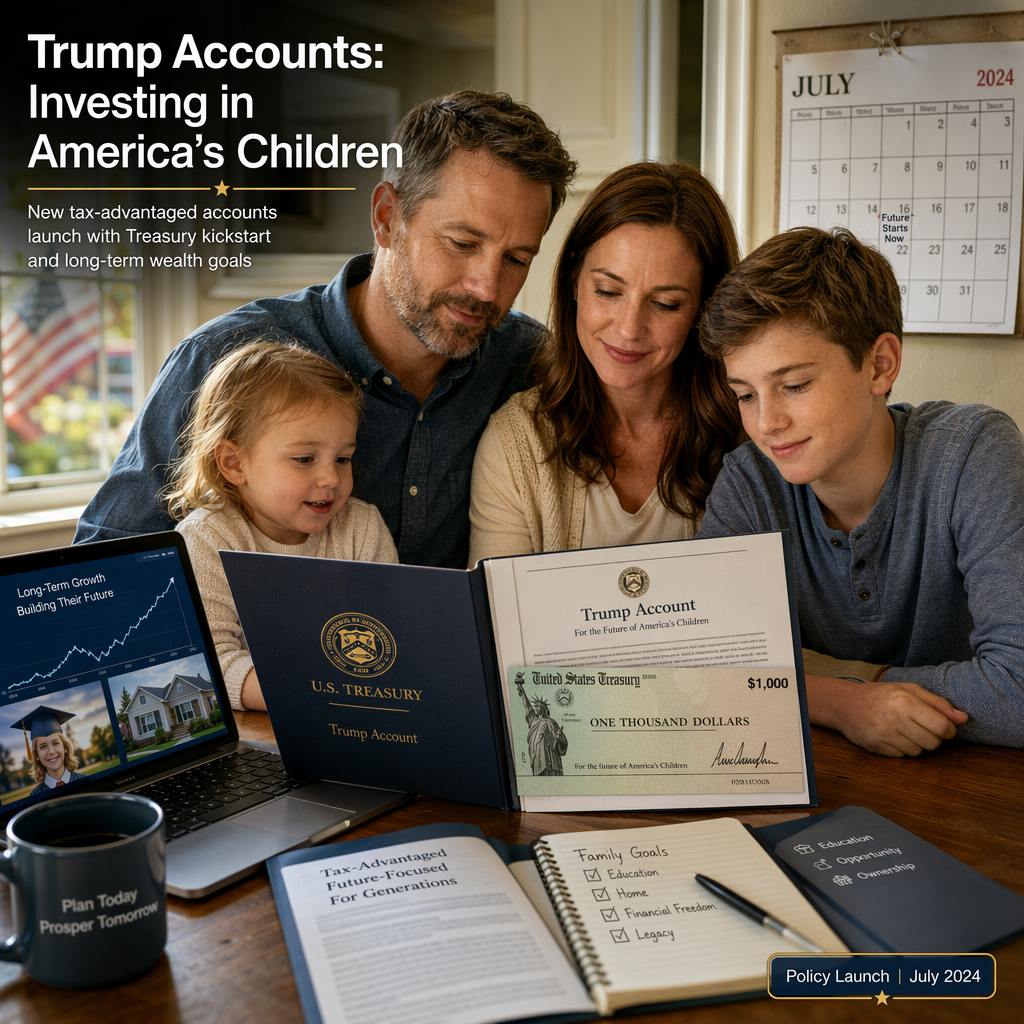

On July 4, Trump Accounts were officially launched, introducing a new tax-advantaged investment vehicle designed specifically for children in the United States [1]. These accounts are intended to help families build long-term wealth for their children, with a focus on retirement savings rather than short-term spending [1]. Eligible children born from 2025 through 2028 can receive a one-time $1,000 contribution from the U.S. Treasury Department after an account is opened [1]. Families are permitted to contribute up to $5,000 per year, with the funds invested in U.S. stock funds and allowed to grow tax-deferred [1].

The program is not limited to parental contributions; employers can contribute up to $2,500 per worker each year, which counts toward the $5,000 annual limit [1]. Additionally, qualifying charities, philanthropists, and state and local governments can make contributions under specified circumstances, and these do not count toward the $5,000 limit [1]. Trump Accounts are available for children aged 18 or younger, and can be opened by parents, legal guardians, grandparents, adult siblings, or other authorized individuals, provided the child is a U.S. citizen with a work-authorized Social Security number [1].

Funds in the Trump Account generally cannot be withdrawn before age 18, at which point the account converts into a traditional Individual Retirement Account (IRA), subject to standard IRA rules [1]. The article provides an example: if a family contributes the maximum $5,000 per year for 18 years and achieves an average annual return of 7 percent, the account could grow to approximately $170,000 by the time the child reaches adulthood [1]. Some of these funds can be used without penalty for college expenses or a home down payment [1].

The article suggests that widespread adoption of Trump Accounts could create a national wealth-building platform supported by families, employers, charities, and local communities [1].

CONCLUSION

The launch of Trump Accounts represents a significant new opportunity for American families to build long-term wealth for their children, with substantial tax advantages and broad eligibility for contributions. If widely adopted, these accounts could have a transformative impact on generational wealth and financial security for future generations.