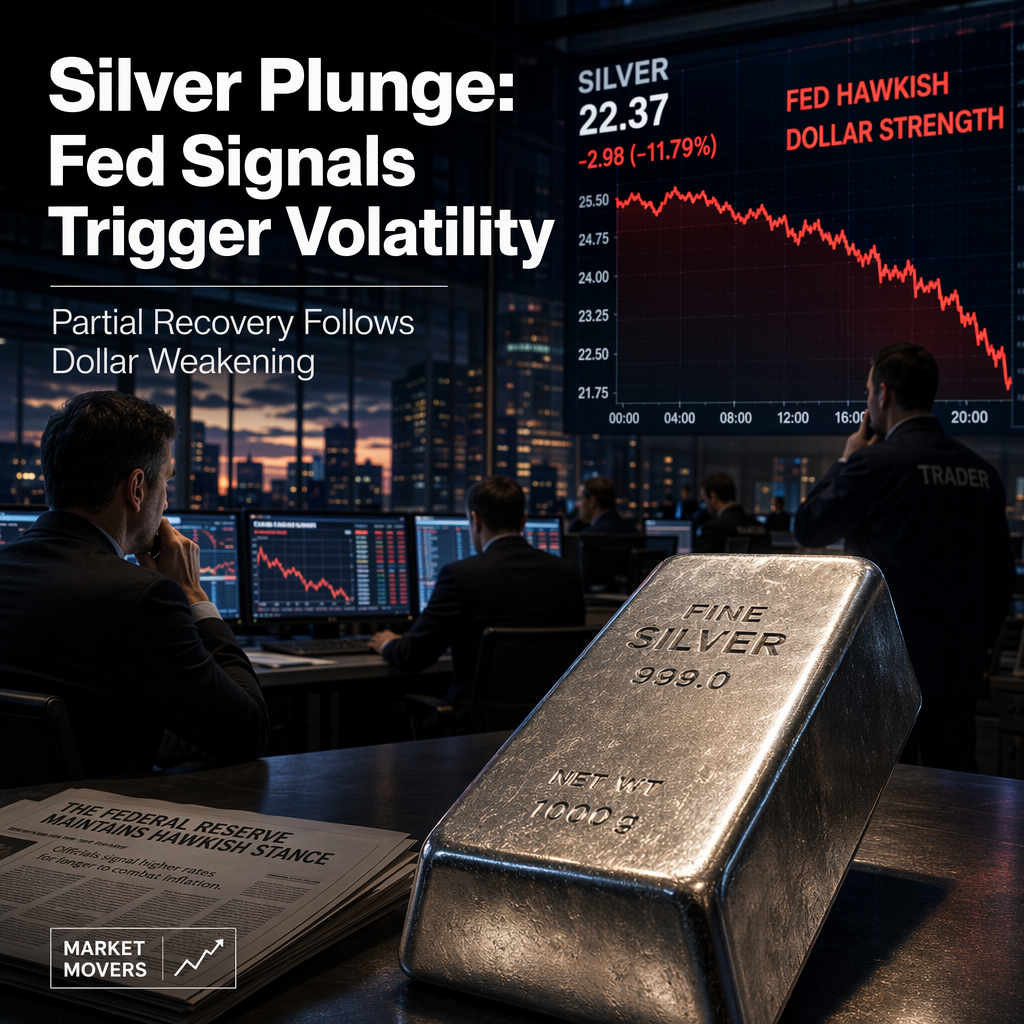

Silver experienced significant volatility this week, opening at $64.85 and dropping nearly 12% over Tuesday and Wednesday due to hawkish Federal Reserve expectations and a stronger U.S. dollar. The metal closed the week at $59.45, marking an 8.78% decline overall [1]. On Monday, silver gained 0.40% to $65.10 following US-Iran talks in Switzerland that produced a 60-day peace roadmap, which eased inflation concerns and rate-hike outlooks. However, the dollar remained strong, topping all major currencies that session, while last week’s hawkish FOMC under Chair Warsh kept real yields elevated [1].

The sharpest declines occurred on Tuesday and Wednesday, with silver falling 5.41% to $61.58 on Tuesday and another 6.75% to $57.42 on Wednesday, totaling an 11.8% drop over those two days. This was attributed to hawkish Fed positioning, which raised real yields and strengthened the dollar, putting downward pressure on silver [1].

A reversal began on Thursday as the Core PCE data came in line with consensus, leading to lower yields and a weaker dollar. Silver responded with a 0.81% gain to $57.89, and the recovery continued on Friday with a 2.18% rise to $59.45 as dollar weakness persisted [1].

The gold/silver ratio widened from 64 to 69 over the week, reflecting silver’s greater volatility compared to gold, which fell 1.60% during the same period. Managed money positioning, as reported by the CFTC, showed a net long of 11,741 contracts, down about 1,200 from the prior week. The report notes that positioning was light and the week’s move was driven by macro factors rather than positioning shifts. The latest COT data is from Tuesday, before the largest drop and subsequent recovery, so further changes in positioning will be reflected in next week’s report [1].

CONCLUSION

Silver saw a sharp midweek selloff driven by hawkish Fed expectations and a stronger dollar, followed by a partial recovery as the dollar weakened. The market reaction was significant, with an 8.78% weekly decline and a notable widening of the gold/silver ratio. Positioning data suggests the move was macro-driven, with further shifts expected to be revealed in upcoming reports.