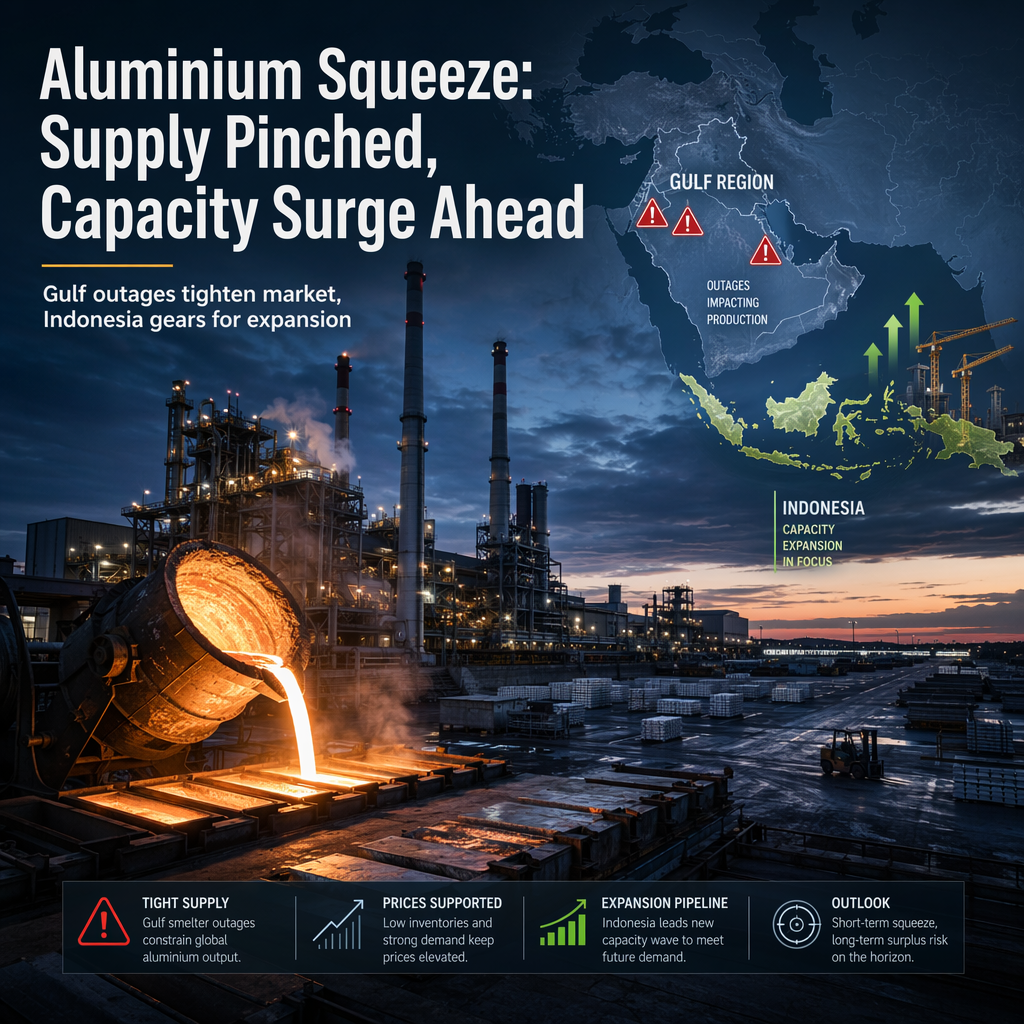

Aluminium prices have rebounded following a recent correction, driven by sharply falling inventories in both China and the London Metal Exchange (LME), as well as ongoing smelter outages in the Gulf region, according to Commerzbank’s Barbara Lambrecht [1]. LME-registered aluminium stocks have dropped below 300,000 tons for the first time since October 2022, and overall stocks could fall below 900,000 tons this month [1].

The Australian Department of Resources and Energy expects the market for primary aluminium to be significantly undersupplied this year and next, citing persistent supply disruptions. While China has partially offset production losses from the Gulf, longer-term outages are anticipated due to damage at regional smelters. Notably, the Al Taweelah smelter in the United Arab Emirates, which has a capacity of 1.6 million tons per year, is expected to be out of operation for 12 months, although the operator recently announced efforts to accelerate the restart [1].

Despite the current tightness, the Australian Ministry projects a more pessimistic long-term outlook. Demand for aluminium is expected to remain robust, supported by the transition to renewable energy, electrification, and increased use in the automotive sector as a substitute for copper. However, supply outside China is forecast to rise sharply, particularly in Indonesia, where capacity is set to expand from 1.3 million tonnes today to 5.3 million tonnes by 2031, driven by increased investment from Chinese investors [1].

While these developments echo recent trends in the nickel industry, the scale is different, and China is expected to maintain its dominant market position [1].

CONCLUSION

Aluminium prices are currently supported by tight supply conditions and ongoing Gulf smelter outages, with inventories at multi-year lows. However, significant capacity expansions, especially in Indonesia, are expected to temper the market's structural outlook in the longer term.