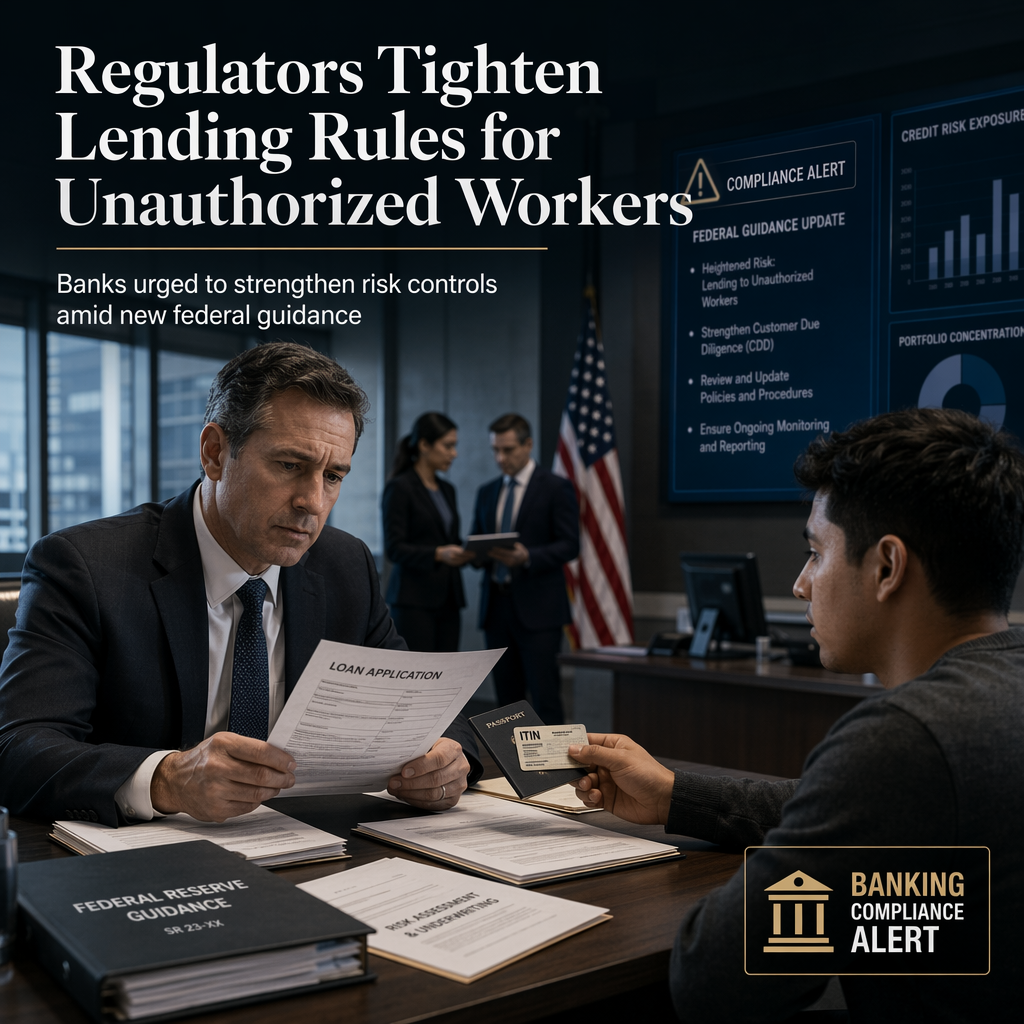

On Monday, the Trump administration, through several financial regulators, issued guidance to banks and credit unions highlighting the credit risks associated with lending to borrowers who are not authorized to work in the United States [1]. The guidance, released by the Office of the Comptroller of the Currency, the Federal Deposit Insurance Corporation, and the National Credit Union Administration, urges financial institutions to identify, measure, monitor, and control these risks through safe underwriting practices [1].

Comptroller of the Currency Jonathan Gould emphasized that the guidance is rooted in existing requirements, stating that financial institutions must consider a prospective borrower's work authorization as part of their risk assessment process [1]. Gould added, "Americans expect their banking system to support lawful business, not facilitate money laundering, or risks associated with criminal illegal immigration" [1]. The guidance reinforces banks' responsibility to know their customers and manage risks, particularly those related to safety, soundness, compliance, and credit when serving individuals not authorized to work in the U.S. [1].

The announcement also references a June guidance from the Consumer Financial Protection Bureau (CFPB), which clarified that financial institutions may consider a consumer's legal ability to work and earn income in the U.S. when making lending decisions, such as for mortgages and credit cards [1]. The CFPB noted that lack of legal work authorization could impact a borrower's income, especially if the applicant is subject to deportation, and that such information can be obtained through direct inquiry or the use of atypical identification methods like an Individual Taxpayer Identification Number (ITIN) [1].

No specific market reactions or analyst opinions were mentioned in the article. However, the guidance signals a tightening of risk management practices for banks and credit unions regarding lending to unauthorized workers [1].

CONCLUSION

Federal regulators have reinforced the need for banks and credit unions to carefully assess the risks of lending to borrowers without legal work authorization in the U.S. The guidance may prompt financial institutions to adopt stricter underwriting standards for such applicants, potentially impacting access to credit for unauthorized workers.