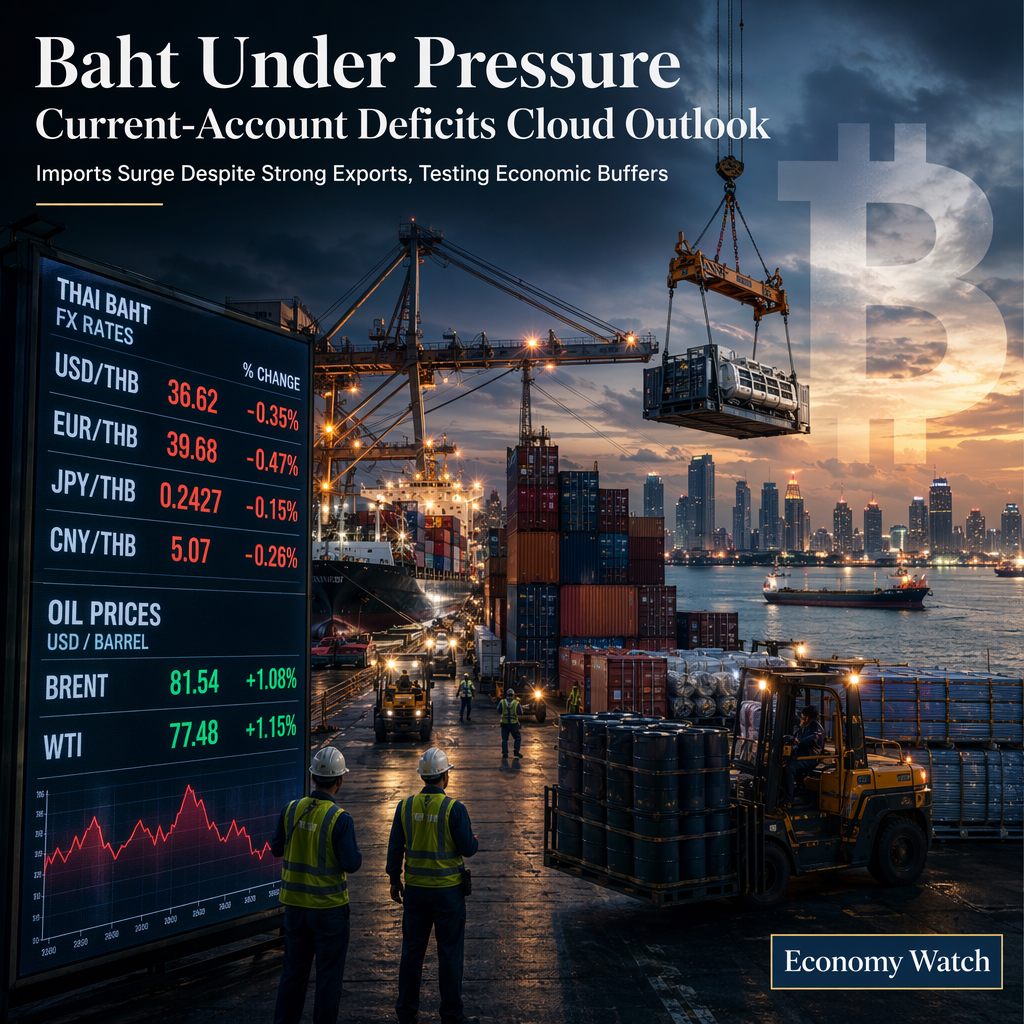

UOB’s Global Economics & Markets Research reports that Thailand’s external buffers remain credible, but the country's current-account dynamics have become less favorable in recent months [1]. Specifically, Thailand recorded current-account deficits in April and May, driven by a surge in imports of energy, raw materials, intermediate goods, and capital goods, while exports remained resilient [1]. This shift means that the current account is no longer providing the same level of comfort as it did earlier in the year, although official reserves remain high and external-debt metrics are still manageable [1].

Inflation in Thailand has also moved quickly back into positive territory, with headline CPI reaching approximately 2.8–2.9% year-on-year in April and May, and producer price pressures remaining elevated [1]. The strong export performance is being offset by equally strong imports, which reduces the domestic value-added multiplier from the export upturn. As a result, the headline trade strength is not fully translating into increased household income, SME revenue, or broad manufacturing output [1].

For financial markets, the Thai baht is expected to remain supported by Thailand’s structural external buffers in the medium term. However, its near-term foreign exchange performance will be sensitive to fluctuations in oil prices, expectations regarding the US Federal Reserve, and upcoming current-account data [1].

CONCLUSION

Thailand’s current-account position has weakened due to a surge in imports, despite resilient exports and strong external buffers. While the baht remains supported by high reserves, its near-term performance is likely to be volatile, influenced by oil prices, Fed expectations, and current-account developments.