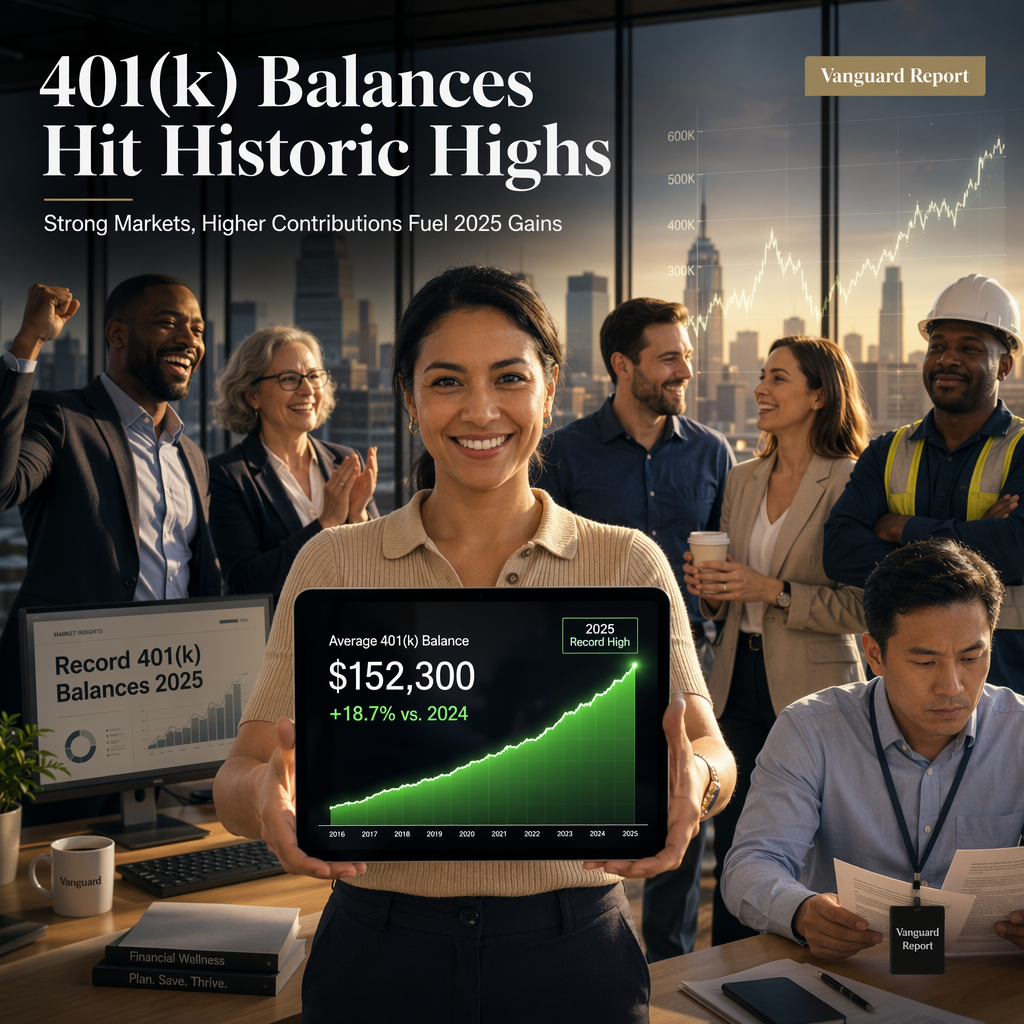

Americans' 401(k) retirement savings accounts reached record levels in 2025, according to a new report from Vanguard titled 'How America Saves 2026' [1]. The report highlights that among employees with active 401(k) accounts in both December 2024 and December 2025, median account balances surged by 27% [1]. Notably, 94% of these participants saw an increase in their account balances, a trend attributed to both higher contributions and robust market returns [1].

The average 401(k) account balance at Vanguard rose to $167,970 in 2025, marking a nearly $20,000 increase from the 2024 average of $148,153 [1]. The median account balance also climbed, rising from $38,176 in 2024 to $44,115 in 2025 [1]. One significant factor contributing to these gains is the growing prevalence of automatic employee enrollment in 401(k) plans. In 2025, 61% of Vanguard-defined contribution plans used automatic enrollment, compared to just 10% in 2006 [1]. This shift has led to stronger participation rates, as employees are now more likely to remain enrolled unless they actively choose to opt out [1].

Employee deferral rates remained steady, with the average deferral at 7.6% of income in both 2024 and 2025, while the median rate was 6.6% in 2025 compared to 6.7% in 2024 [1]. The report also notes that a quarter of all participants deferred more than 10% of their incomes, up from 20% in 2016 [1].

Despite these positive trends, the report points out a rise in hardship withdrawals for the fourth consecutive year, increasing to 6% in 2025 from 5% in 2024 [1]. The report suggests that inflation and other economic pressures may be contributing factors, and that recent streamlining of the hardship withdrawal process has made retirement assets more accessible during times of need [1].

CONCLUSION

Americans' 401(k) balances reached new highs in 2025, driven by increased contributions, strong market performance, and expanded automatic enrollment. However, the rise in hardship withdrawals signals ongoing economic pressures for some participants. Overall, the data reflects both the resilience and challenges facing U.S. retirement savers.