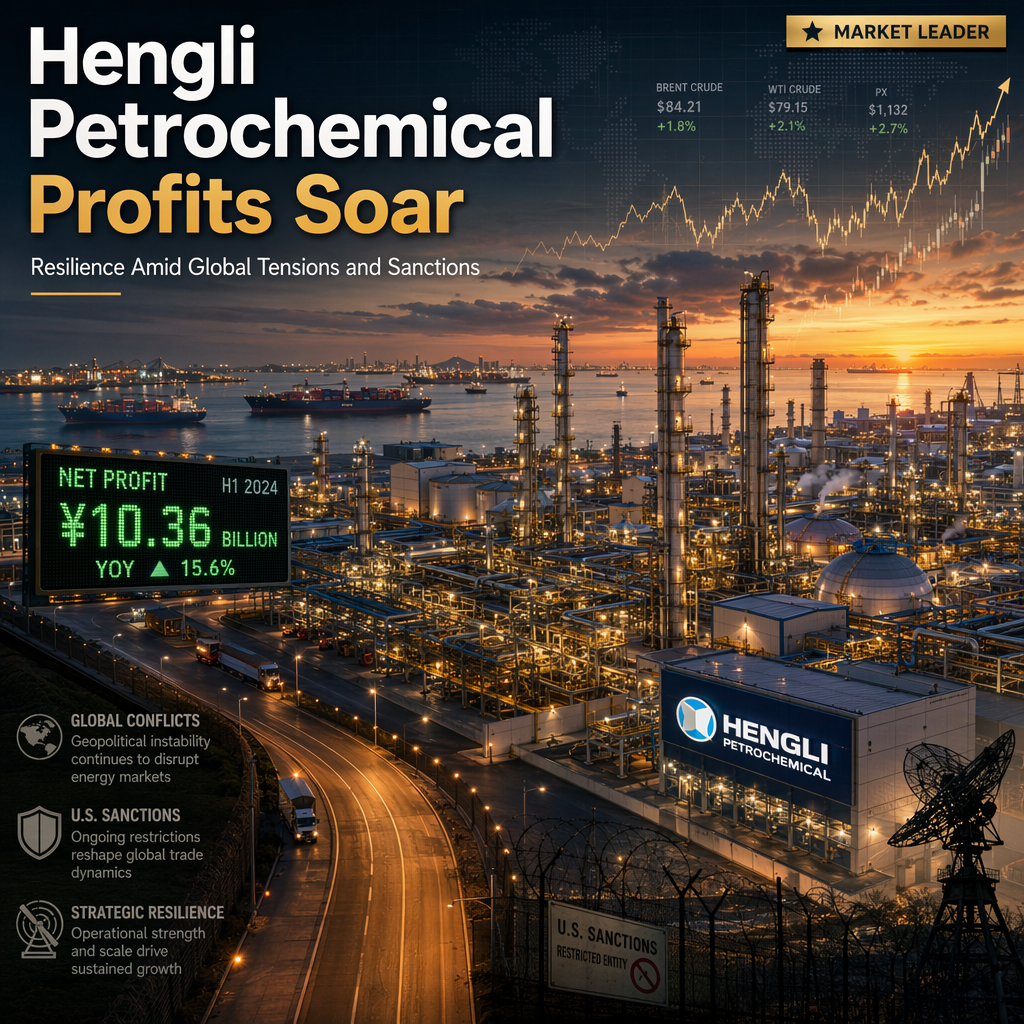

Hengli Petrochemical, a Shanghai-listed parent of a Chinese 'teapot' oil refinery sanctioned by the U.S. for alleged dealings with Iran, reported that its profit more than doubled in the first half of the year, marking a significant spike in earnings for the company and its peers in China's petrochemical sector [1]. The surge in profits is attributed to higher prices for petrochemical products, driven by ongoing global conflicts and supply disruptions, particularly those affecting the Middle East [1]. These elevated commodity prices have buoyed bottom lines across the industry, including key technology suppliers, and reflect robust demand despite international sanctions [1].

Hengli's performance is seen as a leading indicator of the sector's resilience, with other industry players also reporting improved earnings during the same period [1]. Market analysis highlights that the geopolitical tensions have contributed to higher oil and chemical prices, boosting profit margins for Chinese refiners and chemical producers [1].

Analysts maintain a positive outlook for the sector, noting continued price support and the potential for further earnings growth if global tensions persist [1]. Trading advice from market experts emphasizes the importance of monitoring geopolitical developments and commodity price trends, as these factors are expected to continue driving performance in the petrochemical market [1].

CONCLUSION

Hengli Petrochemical's profit doubling underscores the strength of China's petrochemical sector amid global conflicts and U.S. sanctions. Elevated commodity prices have driven robust earnings, and analysts expect continued growth if geopolitical tensions remain. Investors are advised to closely watch global developments and price movements for further market opportunities.